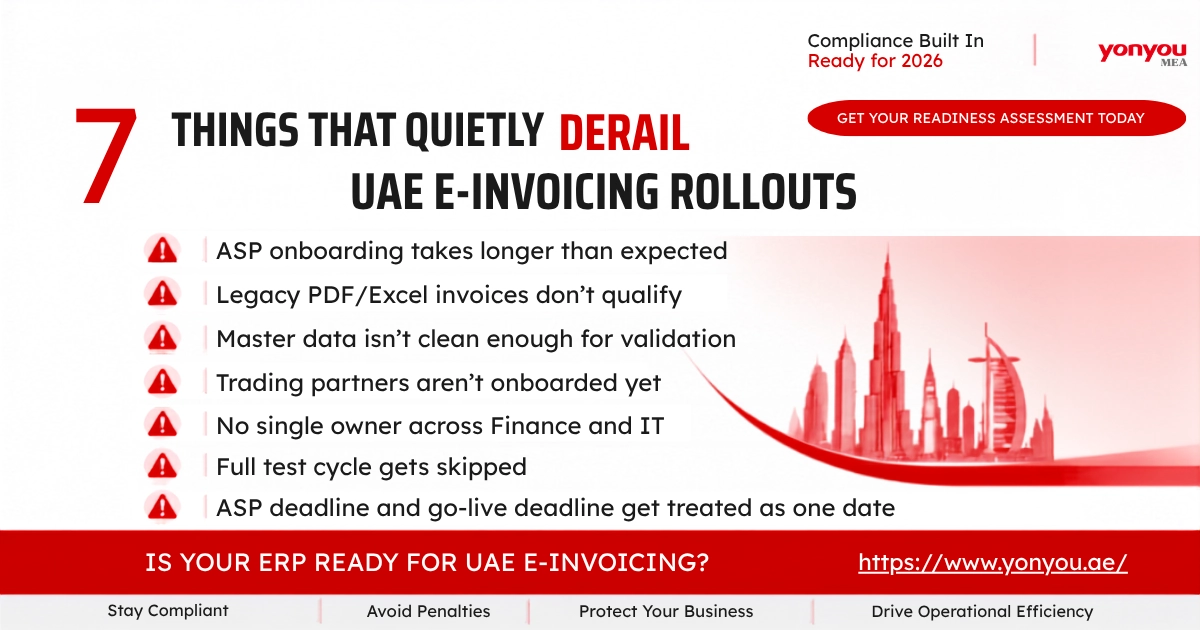

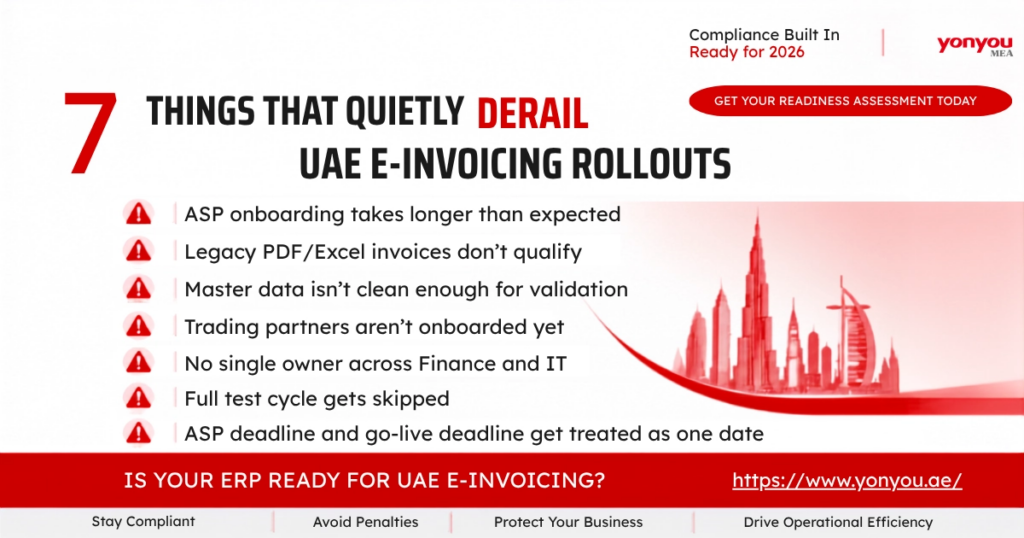

The UAE’s e-invoicing mandate looks straightforward on paper: appoint a provider, connect your system, comply by the deadline. In practice, businesses running their first pilot invoices consistently run into the same seven obstacles. Knowing them in advance is the difference between a smooth rollout and a rushed one.

1. Underestimating ASP selection and onboarding time

Appointing an Accredited Service Provider is not a same-week decision. Businesses need to compare integration compatibility with their existing ERP, per-invoice pricing, and support coverage — then complete a technical onboarding process. Starting this after the ASP deadline has already passed leaves no runway for testing.

2. Legacy invoicing formats that don’t qualify

PDF, scanned images, and Excel invoices are explicitly excluded under the mandate. Businesses still issuing these formats need a structured data pipeline before they can generate a compliant PINT-AE XML invoice — this is often a bigger lift than teams initially expect, especially where invoicing is still partly manual.

3. Master data that isn’t clean enough for validation

Every invoice field — tax codes, customer and supplier identifiers, Peppol participant IDs — has to match the FTA’s data dictionary exactly. Inconsistent or incomplete master data is the leading cause of invoice validation failures during pilot testing.

4. Trading partners who aren’t onboarded yet

Compliance isn’t only about your own systems. If a buyer doesn’t yet have a Peppol participant identifier, suppliers must fall back on predefined endpoints for that transaction type. Coordinating readiness across a customer and supplier base adds a layer of complexity many businesses don’t plan for.

5. No single owner across finance and IT

E-invoicing sits at the intersection of tax compliance, finance operations, and system integration. Where no one person or team owns the project end to end, decisions stall between departments — particularly ASP selection and testing sign-off.

6. Skipping the full test cycle

A compliant setup means testing the entire chain: invoice generation, ASP validation, Peppol transmission, and buyer receipt — not just format conversion in isolation. Errors caught only after the mandatory go-live date risk rejected invoices and delayed payments.

7. Treating the ASP deadline and the go-live deadline as the same date

These are two separate dates with two separate consequences. Businesses that plan only around the mandatory go-live date often miss the earlier ASP appointment deadline, which itself carries its own compliance exposure.

Next in this series: what non-compliance actually costs, and how disruption compounds beyond the fine itself.